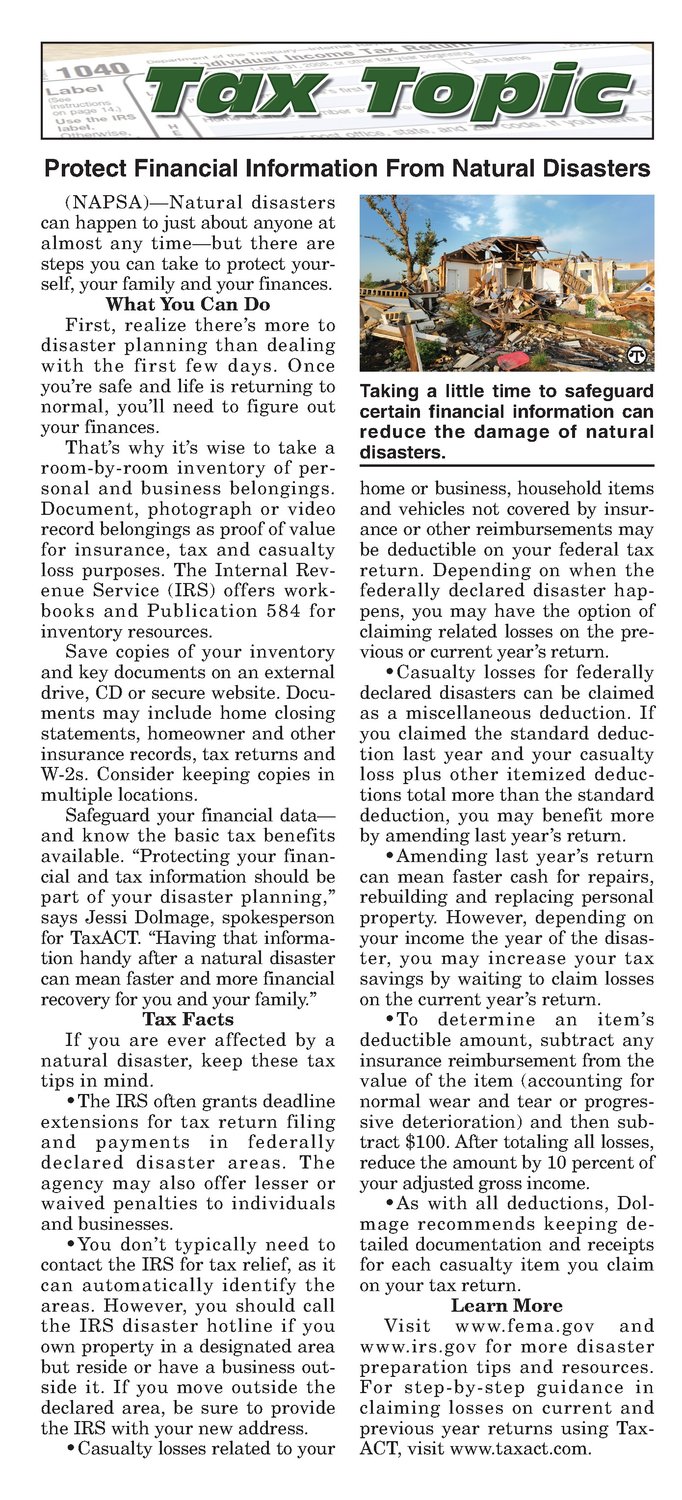

Protect Financial Information From Natural Disasters (NAPSA)—Natural disasters can happen to just about anyone at almost any time—but there are steps you can take to protect your- self, your family and your finances. What You Can Do First, realize there’s more to disaster planning than dealing with the first few days. Once you're safe andlife is returning to normal, you'll need to figure out your finances. That’s why it’s wise to take a room-by-room inventory of per- sonal and business belongings. Document, photograph or video record belongings as proof of value for insurance, tax and casualty loss purposes. The Internal Revenue Service (IRS) offers workbooks and Publication 584 for inventory resources. Save copies of your inventory and key documents on an external drive, CD or secure website. Documents may include homeclosing statements, homeowner and other insurance records, tax returns and W-2s. Consider keeping copies in multiple locations. Safeguard your financial data— and know the basic tax benefits available. “Protecting your financial and tax information should be part of your disaster planning,” says Jessi Dolmage, spokesperson for TaxACT. “Having that information handy after a natural disaster can mean faster and morefinancial recovery for you and yourfamily.” Tax Facts If you are ever affected by a natural disaster, keep these tax tips in mind. The IRS often grants deadline extensions for tax return filing and payments in federally declared disaster areas. The agency mayalso offer lesser or waived penalties to individuals and businesses. *You don’t typically need to contact the IRS for tax relief, as it can automatically identify the areas. However, you should call the IRS disaster hotline if you own property in a designated area but reside or have a business outside it. If you move outside the declared area, be sure to provide the IRS with your new address. * Casualty losses related to your SS SSS Taking a little time to safeguard certain financial information can reduce the damage of natural disasters. homeor business, household items and vehicles not covered by insurance or other reimbursements may be deductible on your federal tax return. Depending on when the federally declared disaster happens, you may have the option of claiming related losses on the previous or current year’s return. Casualty losses for federally declared disasters can be claimed as a miscellaneous deduction. If you claimed the standard deduction last year and your casualty loss plus other itemized deductions total more than the standard deduction, you may benefit more by amending last year’s return. eAmending last year’s return can mean faster cash for repairs, rebuilding and replacing personal property. However, depending on your income the year of the disaster, you may increase your tax savings by waiting to claim losses on the current year’s return. *To determine an item’s deductible amount, subtract any insurance reimbursement from the value of the item (accounting for normal wear and tear or progressive deterioration) and then subtract $100. After totaling all losses, reduce the amount by 10 percent of your adjusted gross income. As with all deductions, Dolmage recommends keeping detailed documentation andreceipts for each casualty item you claim on your tax return. Learn More Visit www.fema.gov and www.irs.gov for more disaster preparation tips and resources. For step-by-step guidance in claiming losses on current and previous year returns using TaxACT,visit www.taxact.com.