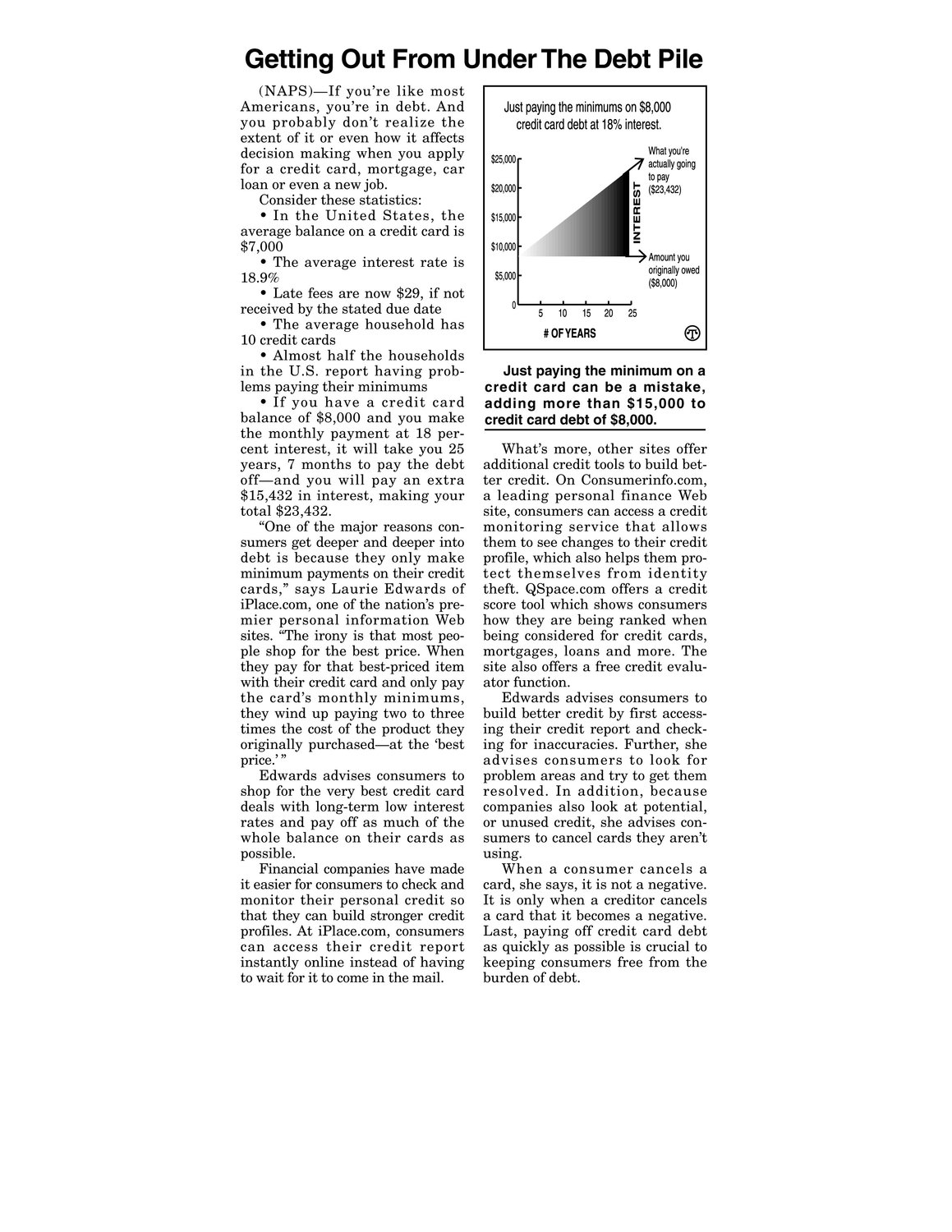

(NAPS)—If you’re like most Americans, you’re in debt. And you probably don’t realize the extent of it or even how it affects decision making when you apply for a credit card, mortgage, car loan or even a newjob. Consider thesestatistics: e In the United States, the average balance on a credit card is Just paying the minimums on $8,000 credit card debt at 18%interest. ($23,432) $15,000 Gi FE z ~ $10,000 18.9% $5,000 e Late fees are now $29, if not received by the stated due date The average household has 10 credit cards Almost half the households in the U.S. report having problems paying their minimums e If you have a credit card balance of $8,000 and you make the monthly payment at 18 percent interest, it will take you 25 actually going to pay $20,000 $7,000 e The average interest rate is Whatyou're $25,000 0 wi Amount you originally owed ($6,000) 5 10 15 20 # OF YEARS 2 @Q Just paying the minimum ona credit card can be a mistake, adding more than $15,000 to credit card debt of $8,000. What’s more, other sites offer years, 7 months to pay the debt off—and you will pay an extra $15,432 in interest, making your total $23,432. “One of the major reasons con- additional credit tools to build bet- debt is because they only make minimum payments ontheir credit profile, which also helps them protect themselves from identity sumers get deeper and deeperinto cards,” says Laurie Edwards of ter credit. On Consumerinfo.com, a leading personal finance Web site, consumerscan accessa credit monitoring service that allows them to see changesto their credit theft. QSpace.com offers a credit iPlace.com, one of the nation’s premier personal information Web score tool which shows consumers how they are being ranked when ple shop for the best price. When they pay for that best-priced item mortgages, loans and more. The sites. “The irony is that most peo- with their credit card and only pay being considered for credit cards, site also offers a free credit evaluator function. the card’s monthly minimums, they wind up paying two to three Edwards advises consumers to build better credit by first access- originally purchased—at the ‘best price.’” Edwards advises consumers to shop for the very best credit card deals with long-term low interest ing for inaccuracies. Further, she times the cost of the product they rates and pay off as much of the whole balance on their cards as possible. Financial companies have made it easier for consumers to check and monitor their personal credit so that they can build stronger credit profiles. At iPlace.com, consumers can access their credit report instantly online instead of having to wait for it to comein the mail. ing their credit report and check- advises consumers to look for problem areas and try to get them resolved. In addition, because companies also look at potential, or unused credit, she advises con- sumers to cancel cards they aren’t using. When a consumer cancels a card, she says, it is not a negative. It is only when a creditor cancels a card that it becomes a negative. Last, paying off credit card debt as quickly as possible is crucial to keeping consumers free from the burden of debt.