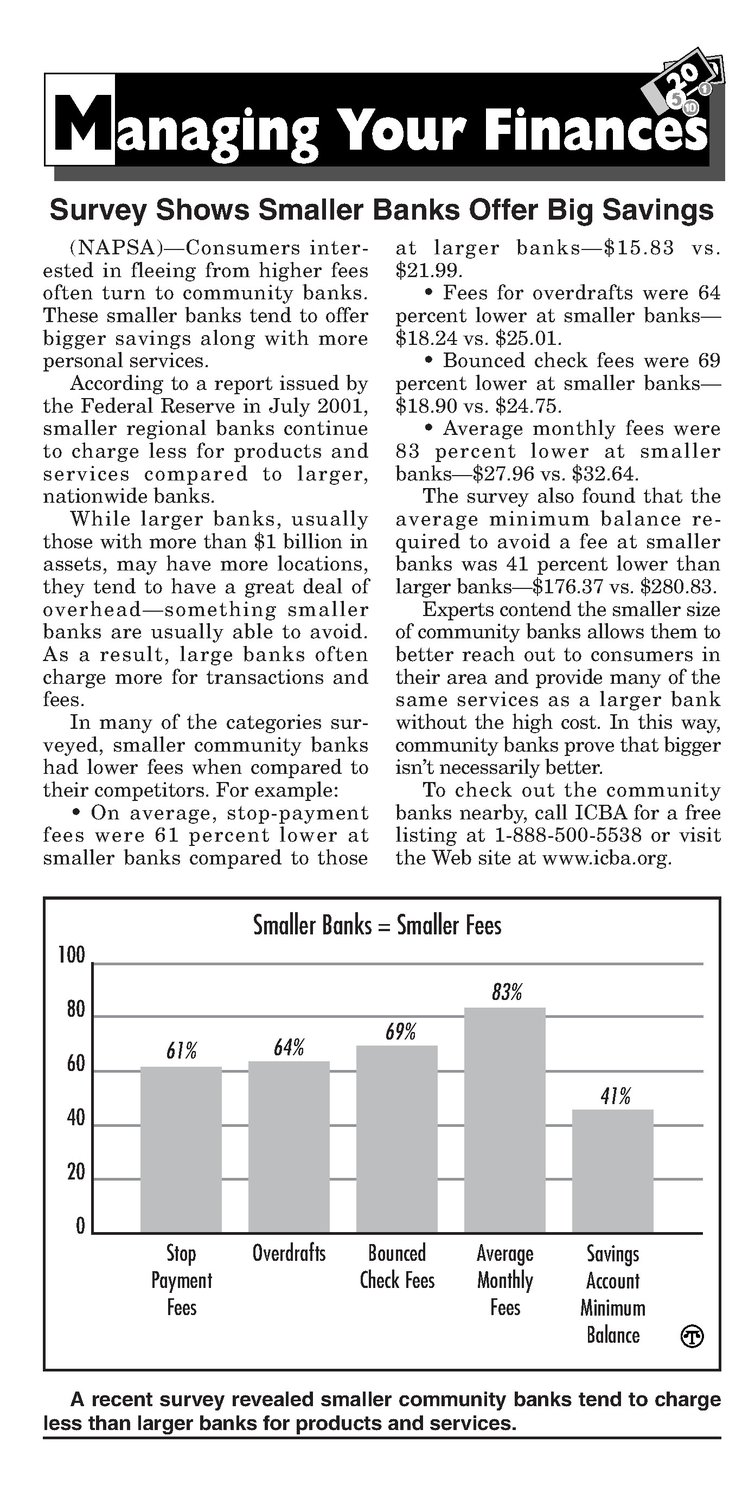

Survey Shows Smaller Banks Offer Big Savings (NAPSA)—Consumers interested in fleeing from higher fees often turn to community banks. These smaller banks tend to offer bigger savings along with more personal services. According to a report issued by the Federal Reserve in July 2001, smaller regional banks continue to charge less for products and services compared to larger, nationwide banks. While larger banks, usually those with more than $1 billion in assets, may have morelocations, they tend to have a great deal of overhead—something smaller banks are usually able to avoid. As a result, large banks often charge more for transactions and fees. In many of the categories surveyed, smaller community banks had lower fees when compared to their competitors. For example: * On average, stop-payment fees were 61 percent lower at smaller banks compared to those $21.99. Fees for overdrafts were 64 percent lower at smaller banks— $18.24 vs. $25.01. * Bounced check fees were 69 percent lower at smaller banks— $18.90 vs. $24.75. Average monthly fees were 83 percent lower at smaller banks—$27.96 vs. $32.64. The survey also found that the average minimum balance required to avoid a fee at smaller banks was 41 percent lower than larger banks—$176.37 vs. $280.83. Experts contend the smaller size of community banksallows them to better reach out to consumers in their area and provide manyof the same services as a larger bank without the high cost. In this way, community banks prove that bigger isn’t necessarily better. To check out the community banks nearby, call ICBA for a free listing at 1-888-500-5538 or visit the Website at www.icba.org. Smaller Banks = Smaller Fees 100 80 40 at larger banks—$15.83 vs. 78 9 61% % 64% 83% 69% 41% 40 20 0 Stop Payment Fees Overdrafts Bounced Check Fees Average Monthly Fees Savings Account Minimum Balance = A recent survey revealed smaller community banks tend to charge less than larger banks for products and services.