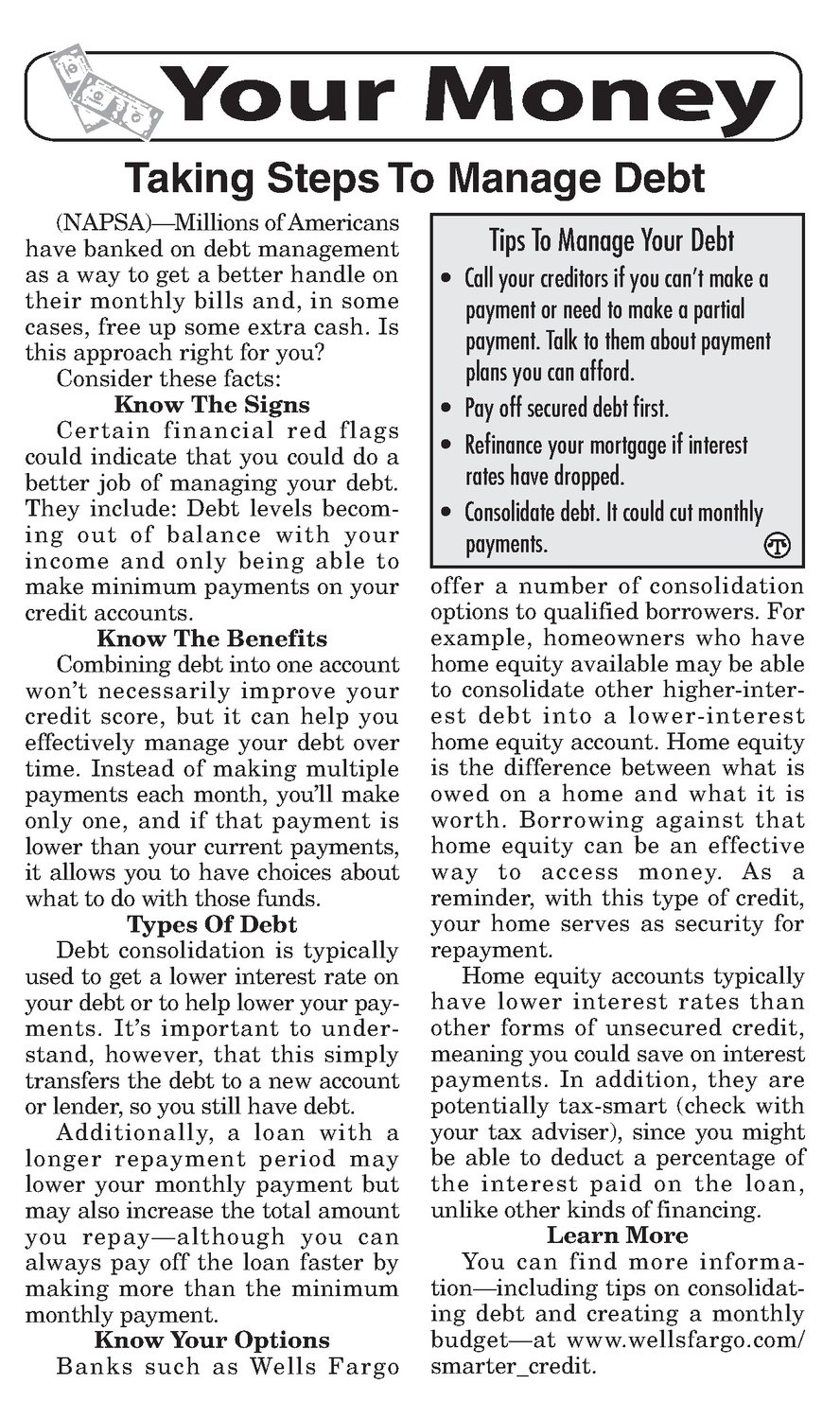

Taking Steps To Manage Debt (NAPSA)—Millions ofAmericans have banked on debt management as a way to get a better handle on their monthly bills and, in some cases, free up some extra cash. Is this approachright for you? Consider these facts: Know The Signs Certain financial red flags could indicate that you could do a better job of managing your debt. They include: Debt levels becoming out of balance with your income and only being able to make minimum payments on your credit accounts. Know TheBenefits Combining debt into one account won’t necessarily improve your credit score, but it can help you effectively manage your debt over time. Instead of making multiple payments each month, you'll make only one, and if that payment is lower than your current payments, it allows you to have choices about what to do with those funds. Types Of Debt Debt consolidation is typically used to get a lower interest rate on your debt or to help lower your payments. It’s important to understand, however, that this simply transfers the debt to a new account or lender, so youstill have debt. Additionally, a loan with a longer repayment period may lower your monthly payment but mayalso increase the total amount you repay—although you can always pay off the loan faster by making more than the minimum monthly payment. Know Your Options Banks such as Wells Fargo Tips To Manage Your Debt Call your creditors if you can’t make a paymentor need to make a partial payment. Talk to them about payment plans you can afford. Pay off secured debtfirst. Refinance your mortgageif interest rates have dropped. Consolidate debt. It could cut monthly payments. @Q offer a number of consolidation options to qualified borrowers. For example, homeowners who have home equity available may be able to consolidate other higher-interest debt into a lower-interest home equity account. Home equity is the difference between what is owed on a home and what it is worth. Borrowing against that home equity can be an effective way to access money. As a reminder, with this type of credit, your homeserves as security for repayment. Home equity accounts typically have lower interest rates than other forms of unsecured credit, meaning you could save on interest payments. In addition, they are potentially tax-smart (check with your tax adviser), since you might be able to deduct a percentage of the interest paid on the loan, unlike other kindsof financing. Learn More You can find more informa- tion—including tips on consolidating debt and creating a monthly budget—at www.wellsfargo.com/ smarter_credit.