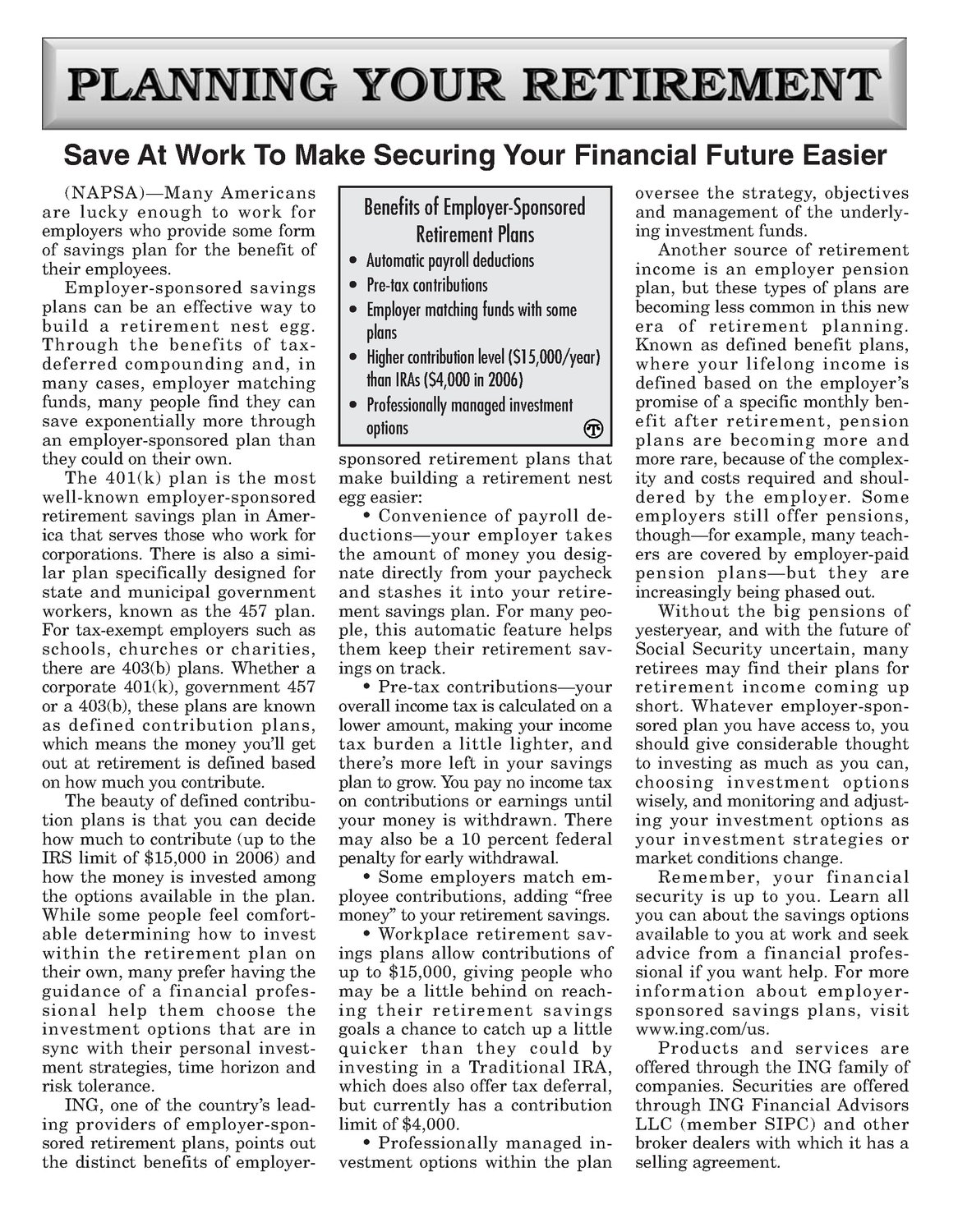

Save At Work To Make Securing Your Financial Future Easier (NAPSA)—Many Americans are lucky enough to work for employers who provide some form of savings plan for the benefit of their employees. Employer-sponsored savings plans can be an effective way to build a retirement nest egg. Through the benefits of taxdeferred compounding and, in many cases, employer matching funds, many people find they can save exponentially more through an employer-sponsored plan than they could on their own. The 401(k) plan is the most well-known employer-sponsored retirement savings plan in America that serves those who work for corporations. There is also a similar plan specifically designed for state and municipal government workers, known as the 457 plan. For tax-exempt employers such as schools, churches or charities, there are 403(b) plans. Whether a corporate 401(k), government 457 or a 403(b), these plans are known as defined contribution plans, which means the money you'll get out at retirement is defined based on how much you contribute. The beauty of defined contribution plans is that you can decide how muchto contribute (up to the IRS limit of $15,000 in 2006) and how the moneyis invested among the options available in the plan. While some people feel comfortable determining how to invest within the retirement plan on their own, many prefer having the guidance of a financial professional help them choose the investment options that are in sync with their personal investment strategies, time horizon and risk tolerance. ING, one of the country’s leading providers of employer-sponsored retirement plans, points out the distinct benefits of employer- Benefits of Employer-Sponsored RetirementPlans Automatic payroll deductions Pre-tox contributions Employer matching funds with some plans e Highercontribution level ($15,000/year) than IRAs ($4,000 in 2006) Professionally managed investment options Gy) sponsored retirement plans that make building a retirement nest egg easier: Convenience of payroll deductions—your employer takes the amount of money you designate directly from your paycheck and stashes it into your retirement savings plan. For many people, this automatic feature helps them keep their retirement savings on track. Pre-tax contributions—your overall incometax is calculated on a lower amount, making your income tax burden a little lighter, and there’s moreleft in your savings plan to grow. You pay no income tax on contributions or earnings until your money is withdrawn. There may also be a 10 percent federal penalty for early withdrawal. Some employers match employee contributions, adding “free money” to your retirement savings. Workplace retirement savings plans allow contributions of up to $15,000, giving people who may be little behind on reaching their retirement savings goals a chance to catch up little quicker than they could by investing in a Traditional IRA, which doesalso offer tax deferral, but currently has a contribution limit of $4,000. Professionally managed investment options within the plan oversee the strategy, objectives and management of the underlying investmentfunds. Another source of retirement income is an employer pension plan, but these types of plans are becoming less commonin this new era of retirement planning. Knownas defined benefit plans, where your lifelong income is defined based on the employer’s promiseof a specific monthly benefit after retirement, pension plans are becoming more and more rare, because of the complexity and costs required and shouldered by the employer. Some employers still offer pensions, though—for example, many teachers are covered by employer-paid pension plans—but they are increasingly being phasedout. Without the big pensions of yesteryear, and with the future of Social Security uncertain, many retirees may find their plans for retirement income coming up short. Whatever employer-sponsored plan you have access to, you should give considerable thought to investing as much as you can, choosing investment options wisely, and monitoring and adjust- ing your investment options as your investment strategies or market conditions change. Remember, your financial security is up to you. Learn all you can about the savings options available to you at work and seek advice from a financial professional if you want help. For more information about employersponsored savings plans, visit www.ing.com/us. Products and services are offered through the ING family of companies. Securities are offered through ING Financial Advisors LLC (member SIPC) and other broker dealers with which it has a selling agreement.