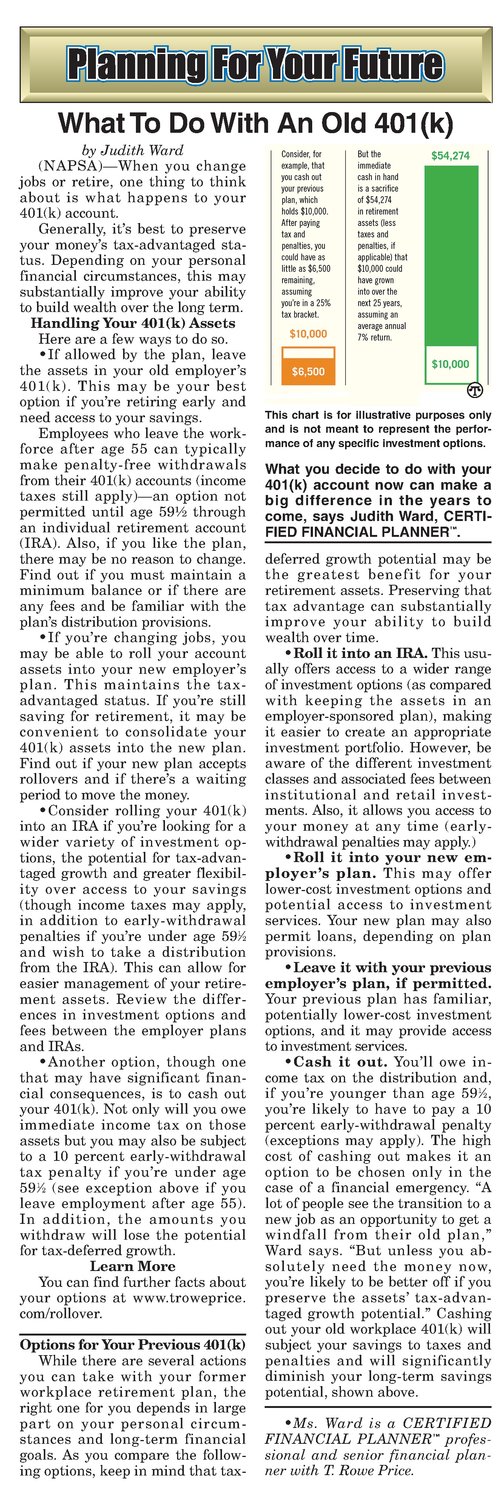

WhatTo Do With An Old 401(k) by Judith Ward (NAPSA)—When you change jobs or retire, one thing to think about is what happens to your 401(k) account. Generally, it’s best to preserve your money’s tax-advantaged status. Depending on your personal financial circumstances, this may substantially improve your ability to build wealth over the long term. Handling Your 401(k) Assets Here are a few waysto do so. eIf allowed by the plan, leave the assets in your old employer’s 401(k). This may be your best option if you're retiring early and need access to your savings. Employees who leave the workforce after age 55 can typically make penalty-free withdrawals from their 401(k) accounts (income taxes still apply)—an option not permitted until age 59% through an individual retirement account (IRA). Also, if you like the plan, there may be no reason to change. Find out if you must maintain a minimum balanceor if there are any fees and be familiar with the plan’s distribution provisions. eIf youre changing jobs, you may be able to roll your account assets into your new employer’s plan. This maintains the taxadvantaged status. If you'restill saving for retirement, it may be convenient to consolidate your 401(k) assets into the new plan. Find out if your new plan accepts rollovers and if there’s a waiting period to move the money. Consider rolling your 401(k) into an IRA if you're looking for a wider variety of investment options, the potential for tax-advantaged growth and greater flexibility over access to your savings (though income taxes may apply, in addition to early-withdrawal penalties if you’re under age 59% and wish to take a distribution from the IRA). This can allow for easier managementof yourretirement assets. Review the differences in investment options and fees between the employer plans and IRAs. Another option, though one that may have significant financial consequences, is to cash out your 401(k). Not only will you owe immediate income tax on those assets but you mayalso be subject to a 10 percent early-withdrawal tax penalty if you’re under age 59% (see exception above if you leave employment after age 55). In addition, the amounts you withdraw will lose the potential for tax-deferred growth. Learn More You can find further facts about your options at www.troweprice. com/rollover. Options for Your Previous 401(k) While there are several actions you can take with your former workplace retirement plan, the right one for you dependsin large part on your personal circumstances and long-term financial goals. As you compare the following options, keep in mindthat tax- Consider, for example, that you cash out your previous plan, which holds $10,000. After paying tax and penalties, you could have as little as $6,500 remaining, assuming you're in a 25% tax bracket. $10,000 But the immediate cash in hand is a sacrifice of $54,274 in retirement assets(less taxes and penalties,if applicable) that $10,000 could have grown into over the next 25 years, assuming an average annual 7% return. Pe ETR $54,274 $10,000 ay This chart is for illustrative purposes only and is not meant to represent the performanceof anyspecific investment options. What you decide to do with your 401(k) account now can make a big difference in the years to come, says Judith Ward, CERTI- FIED FINANCIAL PLANNER™. deferred growth potential may be the greatest benefit for your retirement assets. Preserving that tax advantage can substantially improve your ability to build wealth over time. * Roll it into an IRA.This usually offers access to a wider range of investment options (as compared with keeping the assets in an employer-sponsored plan), making it easier to create an appropriate investment portfolio. However, be aware of the different investment classes and associated fees between institutional and retail investments. Also, it allows you access to your money at any time (earlywithdrawal penalties may apply.) *Roll it into your new employer’s plan. This may offer lower-cost investment options and potential access to investment services. Your new plan may also permit loans, depending on plan provisions. Leave it with your previous employer’s plan, if permitted. Your previous plan has familiar, potentially lower-cost investment options, and it may provide access to investment services. *Cash it out. You'll owe income tax on the distribution and, if you’re younger than age 59%, you're likely to have to pay a 10 percent early-withdrawal penalty (exceptions may apply). The high cost of cashing out makes it an option to be chosen only in the case of a financial emergency. “A lot of people see the transition to a new job as an opportunity to get a windfall from their old plan,” Ward says. “But unless you absolutely need the money now, you're likely to be better off if you preserve the assets’ tax-advantaged growth potential.” Cashing out your old workplace 401(k) will subject your savings to taxes and penalties and will significantly diminish your long-term savings potential, shown above. Ms. Ward is a CERTIFIED FINANCIAL PLANNER”professional and senior financial planner with T. Rowe Price.