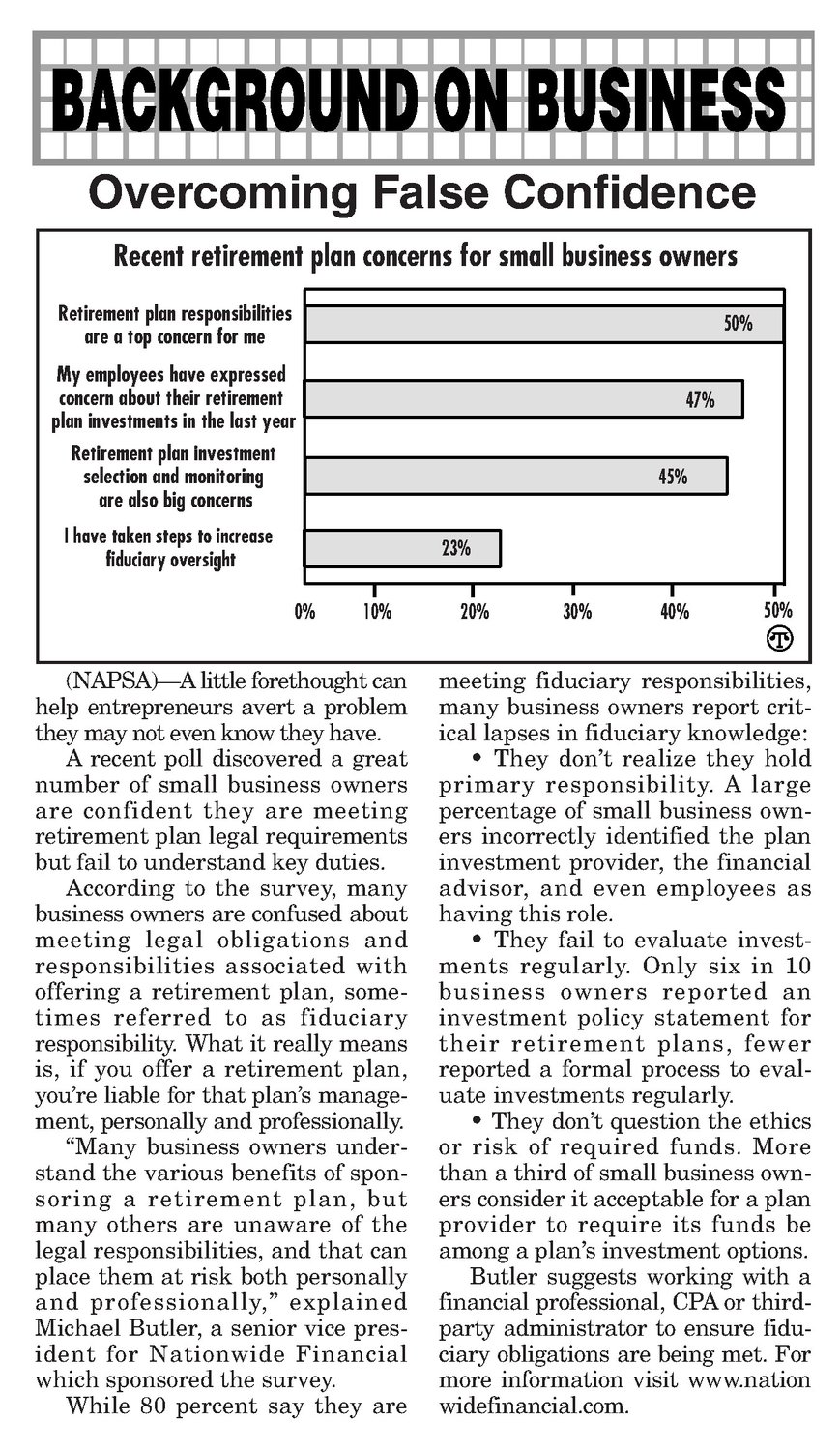

Overcoming False Confidence Recent retirement plan concerns for small business owners Retirement plan responsibilities 50% are a top concern for me My employees have expressed concern abouttheir retirement plan investments in the last year Retirement plan investment selection and monitoring are also big concerns | have taken steps to increase fidudary oversight 23% 0% 10% (NAPSA)—Alittle forethought can help entrepreneurs avert a problem they may not even know they have. A recent poll discovered a great number of small business owners are confident they are meeting retirement plan legal requirements but fail to understand key duties. According to the survey, many business owners are confused about meeting legal obligations and responsibilities associated with offering a retirement plan, sometimes referred to as fiduciary responsibility. What it really means is, if you offer a retirement plan, youre liable for that plan’s management, personally and professionally. “Many business owners understand the various benefits of sponsoring a retirement plan, but many others are unaware of the legal responsibilities, and that can place them at risk both personally and professionally,” explained Michael Butler, a senior vice pres- ident for Nationwide Financial which sponsored the survey. While 80 percent say they are 20% 30% 40% 50% @ meeting fiduciary responsibilities, many business ownersreport critical lapses in fiduciary knowledge: They don’t realize they hold primary responsibility. A large percentage of small business owners incorrectly identified the plan investment provider, the financial advisor, and even employees as having this role. They fail to evaluate investments regularly. Only six in 10 business owners reported an investment policy statement for their retirement plans, fewer reported a formal process to evaluate investments regularly. They don’t question the ethics or risk of required funds. More than a third of small business owners considerit acceptable for a plan provider to require its funds be among a plan’s investmentoptions. Butler suggests working with a financial professional, CPA or thirdparty administrator to ensure fiduciary obligations are being met. For more information visit www.nation widefinancial.com.