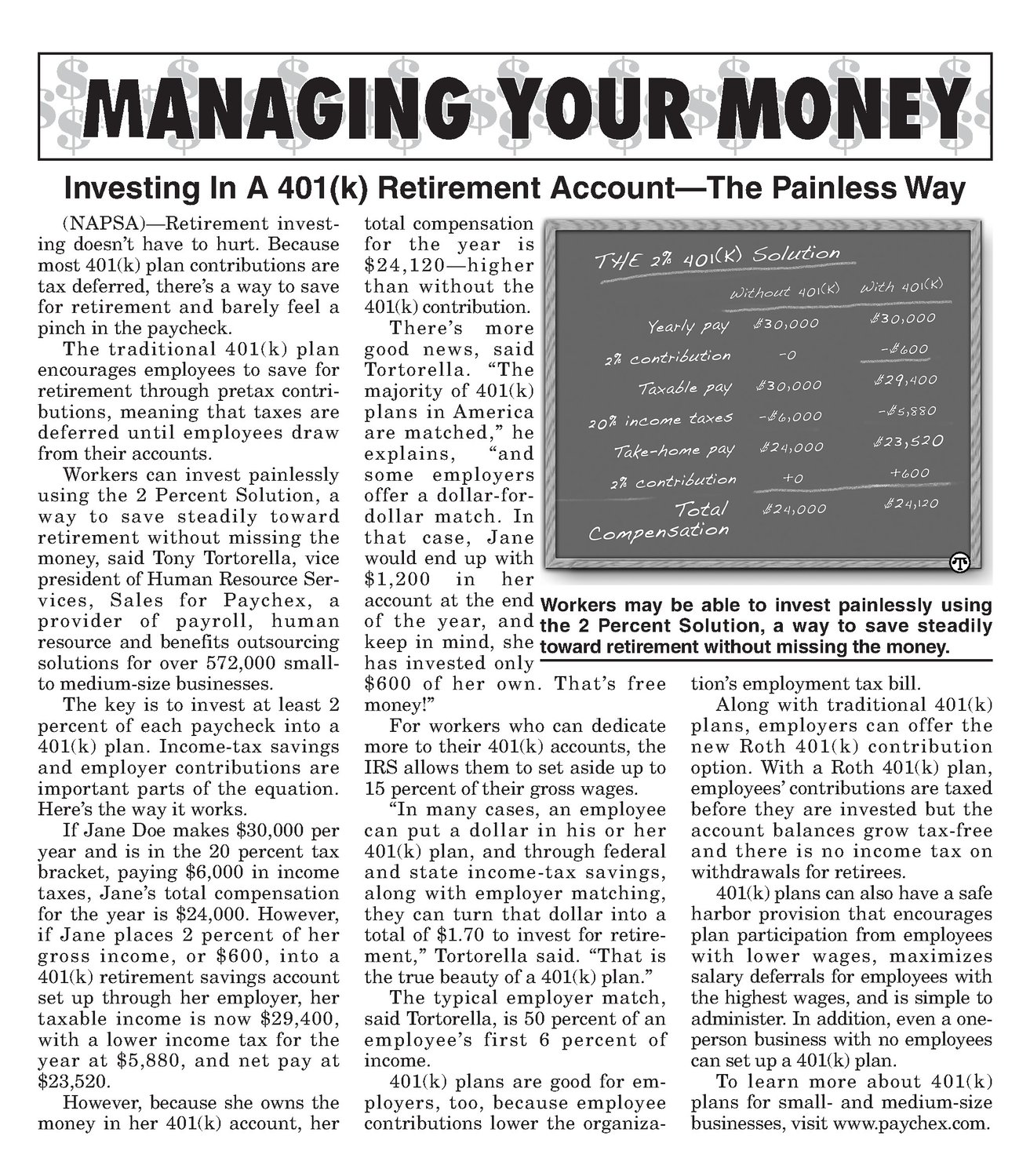

Investing In A 401(k) Retirement Accoun t—The Painless Way (NAPSA)—Retirement investing doesn’t have to hurt. Because most 401(k) plan contributions are tax deferred, there’s a way to save for retirement and barely feel a pinch in the paycheck. The traditional 401(k) plan encourages employees to save for retirement through pretax contributions, meaning that taxes are deferred until employees draw from their accounts. Workers can invest painlessly using the 2 Percent Solution, a way to save steadily toward retirement without missing the money, said Tony Tortorella, vice president of Human Resource Services, Sales for Paychex, a provider of payroll, human resource and benefits outsourcing solutions for over 572,000 smallto medium-size businesses. The key is to invest at least 2 percent of each paycheck into a 401(k) plan. Income-tax savings and employer contributions are important parts of the equation. Here’s the wayit works. If Jane Doe makes $30,000 per year and is in the 20 percent tax bracket, paying $6,000 in income taxes, Jane’s total compensation for the year is $24,000. However, if Jane places 2 percent of her gross income, or $600, into a 401(k) retirement savings account set up through her employer, her taxable income is now $29,400, with a lower income tax for the year at $5,880, and net pay at $23,520. However, because she owns the money in her 401(k) account, her total compensation /-. for the year is || $24,120—higher than without the | 401(k) contribution. | There’s more | good news, said }| Tortorella. “The majority of 401(k) plans in America are matched,” he explains, “and some employers offer a dollar-fordollar match. In that case, Jane | 32s Solutio THE ors goick) area ANG Naha rn 2% contribution 430,000 -0 @ 430,000 Ue EIA $6,000 - $5,330 OLada ae $24,000 423,520 Pyealecaiera iO) WTA ae POY Aa te Ea7me Compensation ELIS ee +600 $24,120 would end up with $1,200 in her account at the end Workers may be able to invest painlessly using of the year, and the 2 Percent Solution, a way to save steadily keep in mind, she toward retirement without missing the money. has invested only $600 of her own. That’s free money!” For workers who can dedicate more to their 401(k) accounts, the IRS allows them to set aside up to 15 percent of their gross wages. “In many cases, an employee can put a dollar in his or her 401(k) plan, and through federal and state income-tax savings, along with employer matching, they can turn that dollar into a total of $1.70 to invest for retirement,” Tortorella said. “That is the true beauty of a 401k) plan.” The typical employer match, said Tortorella, is 50 percent of an employee’s first 6 percent of income. 401(k) plans are good for employers, too, because employee contributions lower the organiza- tion’s employmenttaxbill. Along with traditional 401(k) plans, employers can offer the new Roth 401(k) contribution option. With a Roth 401(k) plan, employees’ contributionsare taxed before they are invested but the account balances grow tax-free and there is no income tax on withdrawals for retirees. 401(k) plans can also have a safe harbor provision that encourages plan participation from employees with lower wages, maximizes salary deferrals for employees with the highest wages, and is simple to administer. In addition, even a one- person business with no employees can set up a 401(k) plan. To learn more about 401(k) plans for small- and medium-size businesses, visit www.paychex.com.