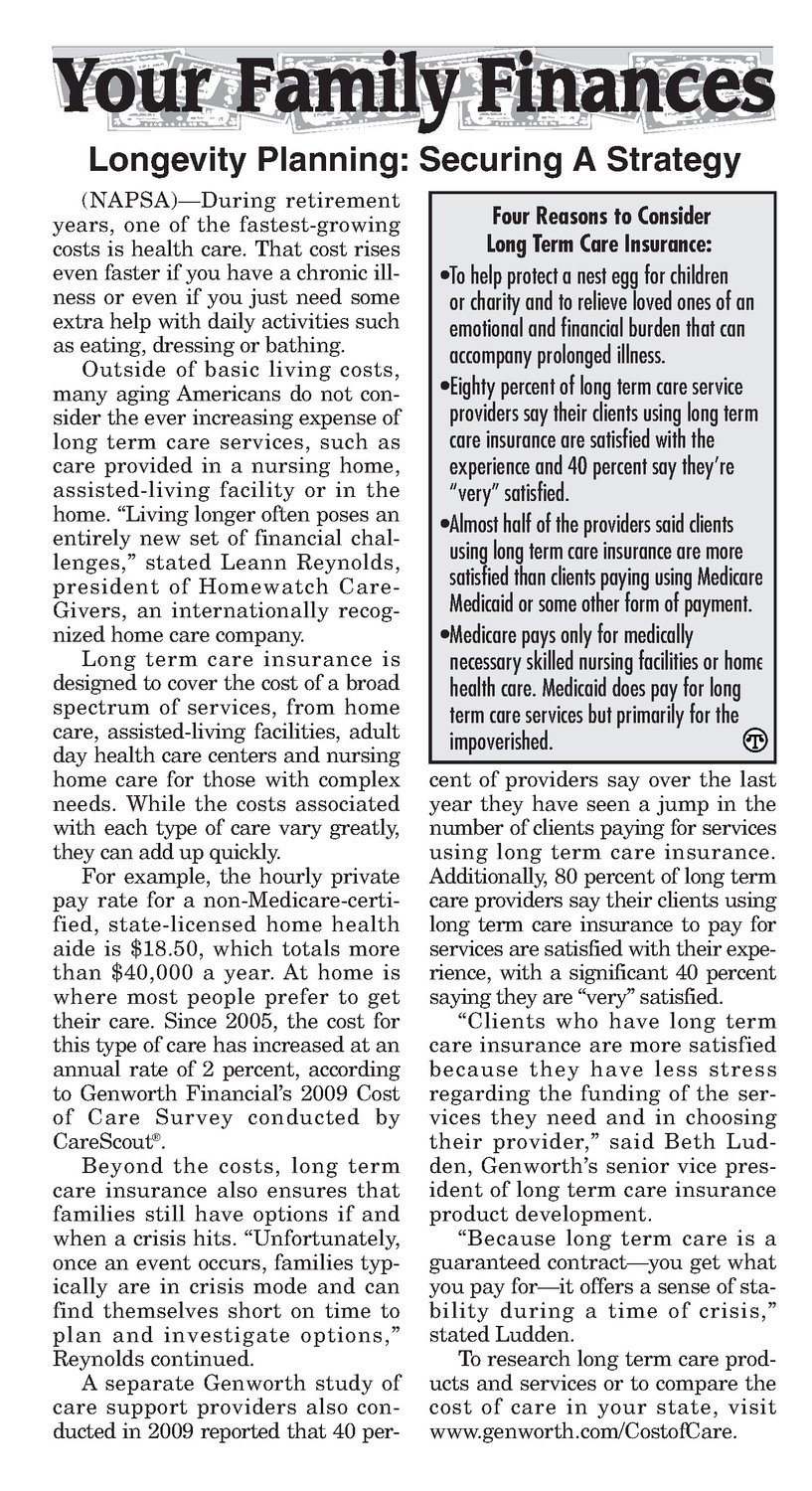

Longevity Planning: Securing A Strategy (NAPSA)—During retirement years, one of the fastest-growing costs is health care. That cost rises even faster if you have a chronic illness or even if you just need some extra help with daily activities such as eating, dressing or bathing. Outside of basic living costs, many aging Americans do not consider the ever increasing expense of long term care services, such as care provided in a nursing home, assisted-living facility or in the home.“Living longer often poses an entirely new set of financial challenges,” stated Leann Reynolds, president of Homewatch CareGivers, an internationally recognized home care company. Long term care insurance is designed to cover the cost of a broad spectrum of services, from home care, assisted-living facilities, adult day health care centers and nursing home care for those with complex needs. While the costs associated with each type of care vary greatly, they can add up quickly. For example, the hourly private pay rate for a non-Medicare-certified, state-licensed home health aide is $18.50, which totals more than $40,000 a year. At home is where most people prefer to get their care. Since 2005, the cost for this type of care has increased at an annual rate of 2 percent, according to Genworth Financial’s 2009 Cost of Care Survey conducted by CareScout. Beyond the costs, long term care insurance also ensures that families still have options if and whena crisis hits. “Unfortunately, once an event occurs, families typically are in crisis mode and can find themselves short on time to plan and investigate options,” Reynolds continued. A separate Genworth study of care support providers also conducted in 2009 reported that 40 per- Four Reasons to Consider Long Term Care Insurance: eTo help protect a nest egg for children or charity and to relieve loved onesof an emotional andfinancial burden that can accompanyprolongedillness. eFighty percent of long term care service providers say their clients using long term core insuranceare satistied with the experience and 40 percent say they're “very”satisfied. eAlmost half of the providers said clients using long term care insurance are more satisfied than clients paying using Medicare Medicaid or some other form of payment. Medicare pays only for medically necessaryskilled nursing facilities or home health care. Medicaid does pay for long term care services but primarily for the impoverished. cent of providers say over thelast year they have seen a jump in the numberof clients paying for services using long term care insurance. Additionally, 80 percent of long term care providers say their clients using long term care insurance to pay for services are satisfied with their experience, with a significant 40 percent saying they are “very”satisfied. “Clients who have long term care insurance are moresatisfied because they have less stress regarding the funding of the services they need and in choosing their provider,” said Beth Ludden, Genworth’s senior vice president of long term care insurance product development. “Because long term care is a guaranteed contract—you get what you pay for—it offers a sense of stability during a time of crisis,” stated Ludden. To research long term care products and services or to compare the cost of care in your state, visit www.genworth.com/CostofCare.