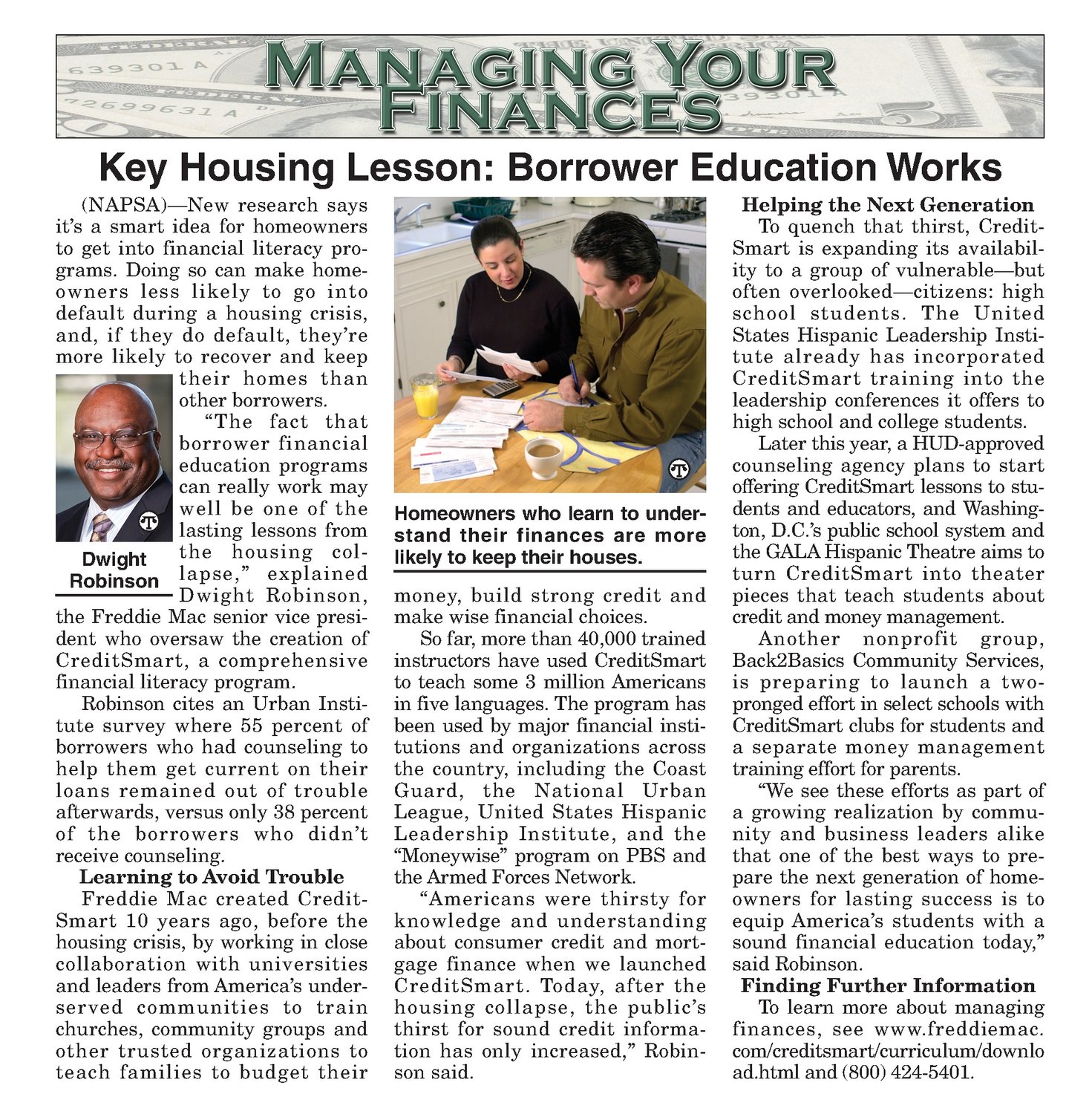

it’s a smart idea for homeowners to get into financial literacy programs. Doing so can make homeowners less likely to go into default during a housingcrisis, and, if they do default, they’re more likely to recover and keep their homes than other borrowers. “The fact that borrower financial education programs can really work may well be one of the lasting lessons from the housing colDwight Robinson lapse,” explained Dwight Robinson, the Freddie Mac senior vice president who oversaw the creation of CreditSmart, a comprehensive financial literacy program. Robinson cites an Urban Institute survey where 55 percent of borrowers who had counseling to help them get current on their loans remained out of trouble afterwards, versusonly 38 percent of the borrowers who didn’t receive counseling. Learning to Avoid Trouble Freddie Mac created CreditSmart 10 years ago, before the housingcrisis, by working in close collaboration with universities andleaders from America’s underserved communities to train churches, community groups and other trusted organizations to teach families to budget their fe i wer Education Works Homeowners wholearn to understand their finances are more likely to keep their houses. money, build strong credit and makewisefinancial choices. So far, more than 40,000 trained instructors have used CreditSmart to teach some 3 million Americans in five languages. The program has been used by major financial institutions and organizations across the country, including the Coast Guard, the National Urban League, United States Hispanic Leadership Institute, and the “Moneywise” program on PBS and the Armed Forces Network. “Americans were thirsty for knowledge and understanding about consumer credit and mortgage finance when we launched CreditSmart. Today, after the housing collapse, the public’s thirst for sound credit information has only increased,” Robinson said. Helping the Next Generation To quench that thirst, CreditSmart is expandingits availability to a group of vulnerable—but often overlooked—citizens: high school students. The United States Hispanic Leadership Institute already has incorporated CreditSmart training into the leadership conferences it offers to high school and college students. Later this year, a HUD-approved counseling agency plans to start offering CreditSmart lessons to students and educators, and Washington, D.C.’s public school system and the GALA Hispanic Theatre aimsto turn CreditSmart into theater pieces that teach students about credit and money management. Another nonprofit group, Back2Basics Community Services, is preparing to launch a twoprongedeffort in select schools with CreditSmartclubs for students and a separate money management training effort for parents. “We see these efforts as part of a growing realization by community and business leaders alike that one of the best ways to prepare the next generation of homeowners for lasting success is to equip America’s students with a sound financial education today,” said Robinson. Finding Further Information To learn more about managing finances, see www.freddiemac. com/creditsmart/curriculum/downlo ad.html and (800) 424-5401.