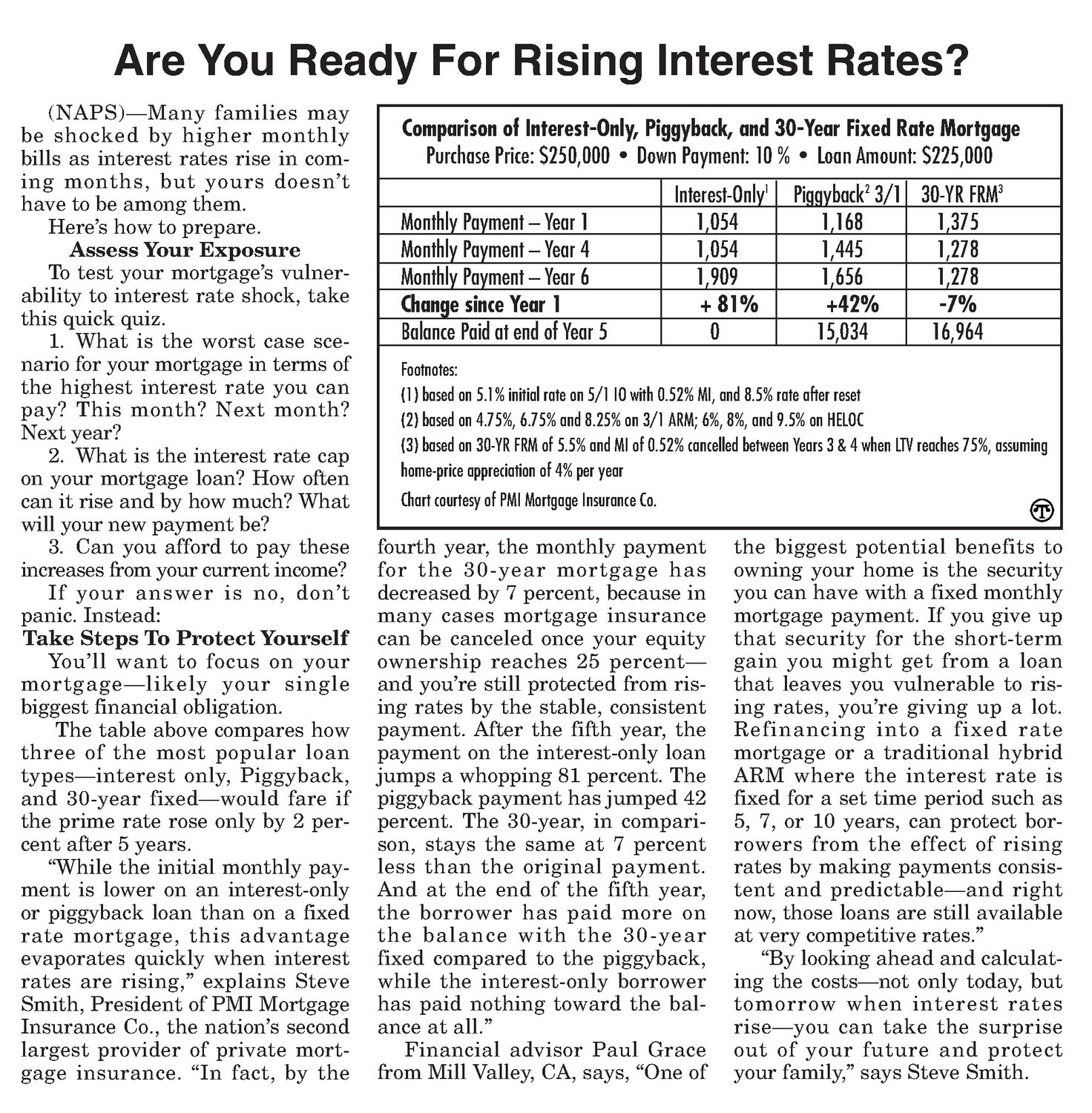

(NAPS)—Many families may be shocked by higher monthly Comparisonof Interest-Only, Piggyback, and 30-Year Fixed Rate Mortgage ing months, but yours doesn’t have to be among them. Here’s how to prepare. Assess Your Exposure Monthly Payment — Year1 bills as interest rates rise in com- To test your mortgage’s vulner- ability to interest rate shock, take this quick quiz. 1. What is the worst case sce- Purchase Price: $250,000 * Down Payment: 10% Loan Amount: $225,000 Monthly Payment — Year 4 Monthly Payment — Year 6 Changesince Year 1 Balance Paid at end of Year 5 Interest-Only'| 1,054 1,054 1,909 + 81% Piggyback? 3/1] 1,168 1,445 1,656 +42% 15,034 30-YR FRM? 1,375 1,278 1,278 7% 16,964 nario for your mortgage in terms of the highest interest rate you can pay? This month? Next month? Next year? 2. What is the interest rate cap on your mortgage loan? How often can it rise and by how much? What will your new payment be? 3. Can you afford to pay these increases from your current income? If your answer is no, don’t panic. Instead: Take Steps To Protect Yourself You'll want to focus on your mortgage—likely your single biggest financial obligation. The table above compares how three of the most popular loan types—interest only, Piggyback, and 30-year fixed—would fare if the prime rate rose only by 2 percent after 5 years. “While the initial monthly payment is lower on an interest-only or piggyback loan than on a fixed rate mortgage, this advantage can be canceled once your equity ownership reaches 25 percent— and you're still protected from rising rates by the stable, consistent payment. After the fifth year, the paymenton the interest-only loan jumps a whopping 81 percent. The piggyback payment has jumped 42 percent. The 30-year, in comparison, stays the same at 7 percent less than the original payment. And at the end of the fifth year, the borrower has paid more on the balance with the 30-year the biggest potential benefits to owning your homeis the security you can have with a fixed monthly mortgage payment. If you give up that security for the short-term gain you might get from a loan that leaves you vulnerable to rising rates, youre giving upa lot. Refinancing into a fixed rate mortgage or a traditional hybrid ARM wherethe interest rate is fixed for a set time period such as 5, 7, or 10 years, can protect borrowers from the effect of rising rates by making payments consistent and predictable—and right now, those loansarestill available at very competitive rates.” rates are rising,” explains Steve Smith, President of PMI Mortgage Insurance Co., the nation’s second largest provider of private mortgage insurance. “In fact, by the while the interest-only borrower has paid nothing toward the balanceat all.” Financial advisor Paul Grace from Mill Valley, CA, says, “One of ing the costs—not only today, but tomorrow when interest rates rise—you can take the surprise out of your future and protect your family,” says Steve Smith. evaporates quickly when interest Footnotes: (1) based on 5.1% initial rate on 5/1 10 with 0.52% MI, and 8.5% rate after reset (2) based on 4.75%, 6.75% and 8.25% on 3/1 ARM; 6%, 8%, and 9.5% on HELOC (3) based on 30-YR FRM of 5.5% and MI of 0.52% cancelled between Years 3 & 4 when LTV reaches 75%, assuming home-price appreciation of 4% per year Chart courtesy of PMI Morigage Insurance Co. fourth year, the monthly payment for the 30-year mortgage has decreased by 7 percent, because in many cases mortgage insurance fixed compared to the piggyback, @ “By looking ahead andcalculat-