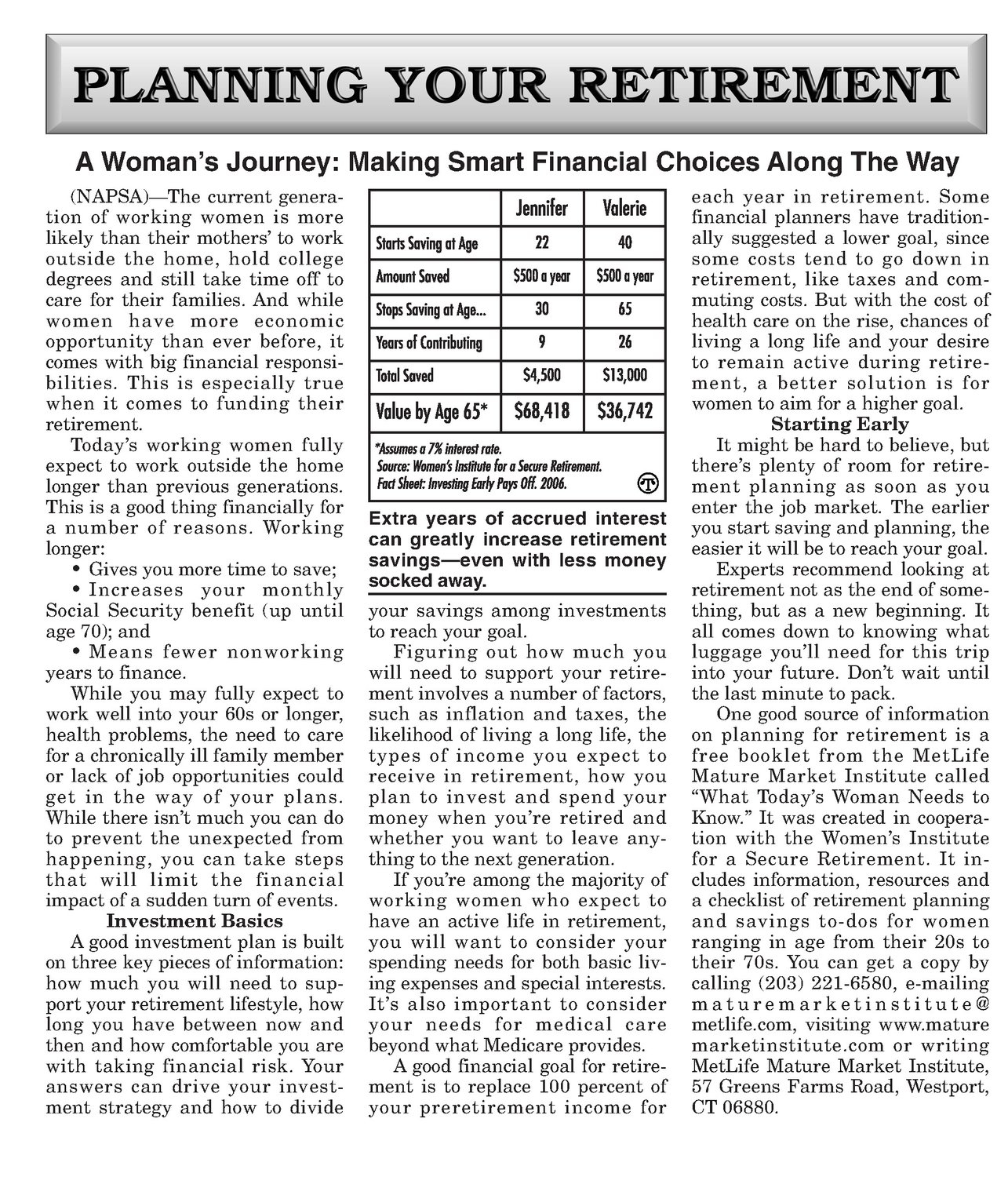

A Woman’s Journey: Making Smart Financial Choices Along The Way (NAPSA)—Thecurrent generation of working women is more likely than their mothers’ to work outside the home, hold college degrees and still take timeoff to care for their families. And while women have more economic opportunity than ever before, it comes with big financial responsibilities. This is especially true when it comes to funding their retirement. Today’s working women fully expect to work outside the home longer than previous generations. This is a good thing financially for a number of reasons. Working longer: Gives you more timeto save; Increases your monthly Social Security benefit (up until age 70); and * Means fewer nonworking yearsto finance. While you may fully expect to work well into your 60s or longer, health problems, the need to care for a chronically ill family member or lack of job opportunities could get in the way of your plans. While there isn’t much you can do to prevent the unexpected from happening, you can take steps that will limit the financial impact of a sudden turnof events. Investment Basics A good investment planis built on three key pieces of information: how much you will need to support your retirementlifestyle, how long you have between now and then and how comfortable you are with taking financial risk. Your answers can drive your invest- ment strategy and how to divide Jennifer Valerie 22 40 $5000 year $500 ayear Stops Saving of Age... 30 65 Yearsof Contributing 9 26 $4,500 $13,000 $68,418 $36,742 Starts Saving at Age Amount Saved Total Saved Value by Age 65* “Assumes a 7% interest rate, Source: Women’s Institute for a Secure Retirement, Fact Shoot: investing Early Pays Off. 2006. Extra years of accrued interest can greatly increase retirement savings—even with less money socked away. your savings among investments to reach yourgoal. Figuring out how much you will need to support your retirement involves a numberoffactors, such as inflation and taxes, the likelihood of living a long life, the types of income you expect to receive in retirement, how you plan to invest and spend your money when you’re retired and whether you want to leave anything to the next generation. If youw’re among the majority of working women who expect to have an active life in retirement, you will want to consider your spending needs for both basic living expenses andspecialinterests. It’s also important to consider your needs for medical care beyond what Medicare provides. A good financial goal for retirement is to replace 100 percent of your preretirement income for each year in retirement. Some financial planners have traditionally suggested a lower goal, since some costs tend to go down in retirement, like taxes and commuting costs. But with the cost of health care on the rise, chances of living a long life and your desire to remain active during retire- ment, a better solution is for womento aim for a highergoal. Starting Early It might be hard to believe, but there’s plenty of room for retirement planning as soon as you enter the job market. The earlier you start saving and planning, the easier it will be to reach your goal. Experts recommend looking at retirement not as the end of something, but as a new beginning. It all comes down to knowing what luggage you'll need for this trip into your future. Don’t wait until the last minute to pack. One good source of information on planning for retirement is a free booklet from the MetLife Mature Market Institute called “What Today’s Woman Needs to Know.” It was created in cooperation with the Women’s Institute for a Secure Retirement. It in- cludes information, resources and a checklist of retirement planning and savings to-dos for women ranging in age from their 20s to their 70s. You can get a copy by calling (203) 221-6580, e-mailing maturemarketinstitute@ metlife.com, visiting www.mature marketinstitute.com or writing MetLife Mature Market Institute, 57 Greens Farms Road, Westport, CT 06880.