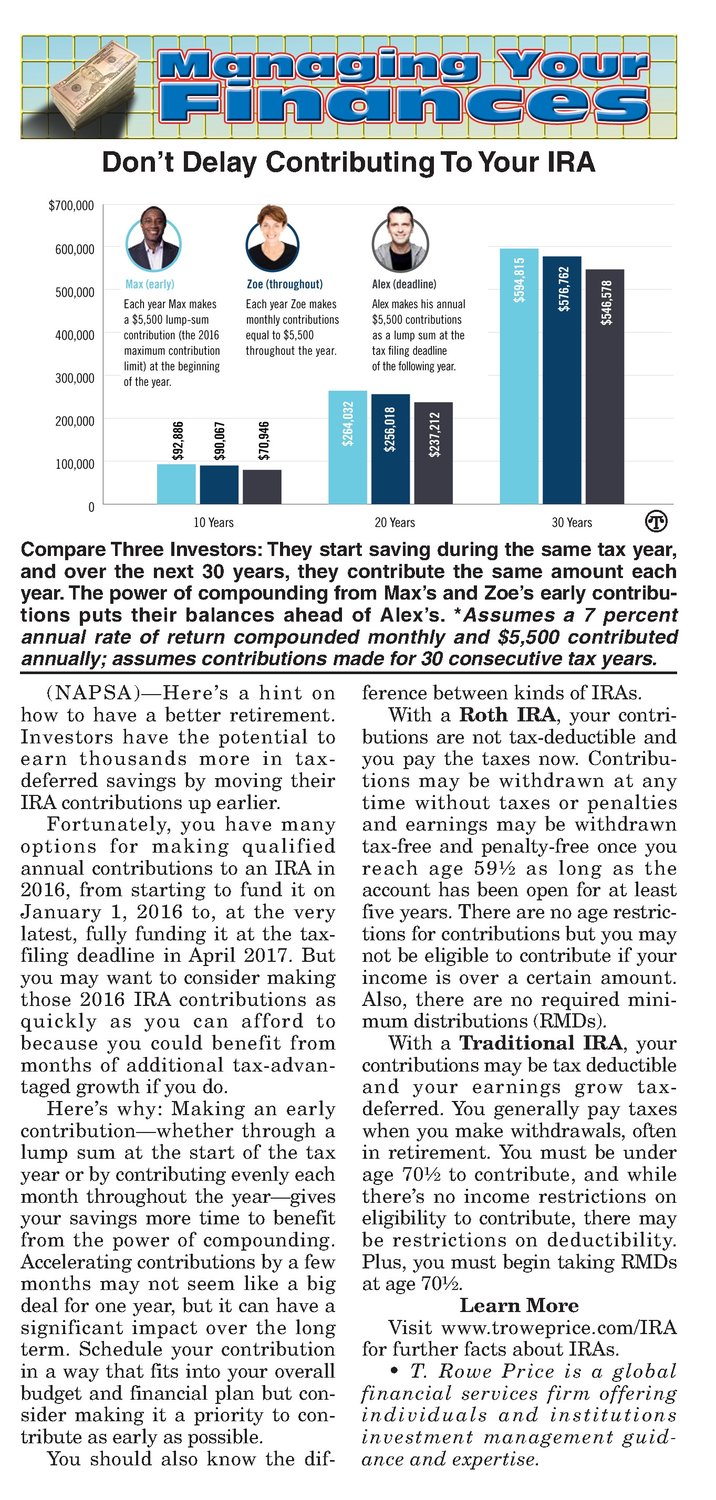

$700,000 nen 500,000 400,000 300,000 $ Oo Max (early) Zoe(throughout) Alex (deadline) Each year Max makes a $5,500 lump-sum contribution (the 2016 maximum contribution limit) at the beginning of the year. Each year Zoe makes monthly contributions equal to $5,500 throughout the year. Alex makes his annual $5,500 contributions as a lump sum at the taxfiling deadline of thefollowing year. 200,000 100,000 0 10 Years 20 Years 30 Years @ Compare Three Investors: They start saving during the same tax year, and over the next 30 years, they contribute the same amount each year. The power of compounding from Max’s and Zoe’s early contributions puts their balances ahead of Alex’s. *Assumes a 7 percent annualrate of return compounded monthly and $5,500 contributed annually; assumes contributions made for 30 consecutive tax years. (NAPSA)—Here’s a hint on how to have a better retirement. Investors have the potential to earn thousands more in taxdeferred savings by moving their IRA contributions upearlier. Fortunately, you have many options for making qualified annual contributions to an IRA in 2016, from starting to fund it on January 1, 2016 to, at the very latest, fully funding it at the taxfiling deadline in April 2017. But you may want to consider making those 2016 IRA contributions as quickly as you can afford to because you could benefit from months of additional tax-advantaged growthif you do. Here’s why: Making an early contribution—whether through a lump sum at the start of the tax year or by contributing evenly each month throughout the year—gives your savings more time to benefit from the power of compounding. Accelerating contributions by a few months may not seem like a big deal for one year, but it can have a significant impact over the long term. Schedule your contribution in a waythatfits into your overall budget and financial plan but consider making it a priority to contribute as early as possible. You should also know the dif- ference between kindsof IRAs. With a Roth IRA, your contributions are not tax-deductible and you pay the taxes now. Contributions may be withdrawn at any time without taxes or penalties and earnings may be withdrawn tax-free and penalty-free once you reach age 59% as long as the account has been open for at least five years. There are no agerestrictions for contributions but you may not be eligible to contribute if your incomeis over a certain amount. Also, there are no required minimum distributions (RMDs). With a Traditional TRA, your contributions may be tax deductible and your earnings grow taxdeferred. You generally pay taxes when you make withdrawals, often in retirement. You must be under age 70% to contribute, and while there’s no incomerestrictions on eligibility to contribute, there may be restrictions on deductibility. Plus, you must begin taking RMDs at age 70%. Learn More Visit www.troweprice.com/IRA for further facts about IRAs. T. Rowe Price is a global financial services firm offering individuals and institutions investment management guidance and expertise.